Living on a limited income can make saving money feel impossible. Rising living costs, rent, groceries, transportation, and unexpected expenses often leave little room for financial growth. However, learning how to save money fast on a low income is not about earning a six-figure salary—it is about making strategic decisions, controlling spending habits, and creating systems that help you keep more of what you earn.

Many people assume that saving money requires major sacrifices, but small changes can create significant results over time. Whether you are living paycheck to paycheck, supporting a family, paying off debt, or simply trying to build an emergency fund, there are proven methods that can help you save faster than you think.

The key is focusing on high-impact actions instead of trying dozens of complicated budgeting techniques. By reducing unnecessary expenses, increasing financial awareness, and automating good money habits, even individuals with modest incomes can achieve meaningful savings goals.

This guide explains practical, realistic, and actionable ways to save money quickly while earning a low income. You’ll discover strategies used by financial experts, real-world examples, common mistakes to avoid, and a step-by-step plan to improve your financial situation starting today.

Quick Answer

If you want to save money fast on a low income:

- Create a realistic budget.

- Track every expense.

- Cut non-essential spending.

- Reduce housing and transportation costs.

- Automate savings transfers.

- Build an emergency fund.

- Avoid high-interest debt.

- Increase income through side hustles.

- Use cash-back and discount programs.

- Set clear savings goals.

The fastest results usually come from reducing major expenses and consistently saving small amounts every week.

Key Takeaways

- Saving money is possible even with limited income.

- Small daily savings can add up significantly over time.

- Budgeting helps identify spending leaks.

- Emergency funds prevent financial setbacks.

- Debt reduction increases available cash flow.

- Automation removes the temptation to spend.

- Additional income sources accelerate savings goals.

- Long-term consistency matters more than perfection.

Table of Contents

- How to Save Money Fast on a Low Income: Why It Matters

- Best Budgeting Strategies to Save Money Fast on a Low Income

- Ways to Save Money Fast on a Low Income by Reducing Expenses

- Step-by-Step Guide to Save Money Fast on a Low Income

- Expense Comparison for Low-Income Money Saving Strategies

- Real Examples of People Saving Money Fast on a Low Income

- Benefits of Learning How to Save Money Fast on a Low Income

- Challenges When Trying to Save Money Fast on a Low Income

- Common Mistakes That Prevent Fast Saving on a Low Income

- Expert Tips to Save Money Fast on a Low Income

- Frequently Asked Questions

- Final Verdict

How to Save Money Fast on a Low Income: Why It Matters

Financial security begins with having money set aside for unexpected situations. Unfortunately, people with lower incomes often face greater financial vulnerability because even a minor emergency can disrupt their entire budget.

When you have little or no savings, events such as medical bills, car repairs, home maintenance costs, or temporary job loss can force you into debt. This creates a cycle where future income is spent repaying past emergencies instead of building wealth.

Saving money quickly provides several immediate benefits. First, it creates peace of mind. Knowing that you have funds available for emergencies reduces financial stress and improves decision-making. Second, savings help prevent reliance on credit cards and payday loans, which often carry high interest rates.

Many households underestimate the importance of small savings milestones. Even accumulating $500 to $1,000 can dramatically improve financial stability. Once that foundation is established, larger goals such as debt repayment, home ownership, education funding, or retirement investing become more achievable.

How Consistent Saving Helps Low-Income Households

One common misconception is that meaningful savings require large deposits. In reality, consistency often matters more than the amount saved.

For example, saving just $10 per day results in approximately $300 per month and $3,650 annually. While this may seem modest, it demonstrates how small actions compound over time.

Consistency also strengthens financial discipline. When saving becomes a habit rather than an occasional activity, long-term success becomes much more likely. Developing routines such as automatic transfers, weekly expense reviews, and spending limits creates sustainable progress regardless of income level.

Best Budgeting Strategies to Save Money Fast on a Low Income

The foundation of every successful savings plan is a budget. Budgeting provides visibility into where your money goes and identifies opportunities to reduce unnecessary spending.

Many people avoid budgeting because they believe it is restrictive. However, an effective budget is simply a financial roadmap that aligns spending with priorities.

A practical starting point is tracking every expense for one month. This process often reveals surprising spending patterns, including subscription services, impulse purchases, convenience spending, and dining expenses that gradually consume a large portion of income.

The process of how to save money becomes easier when every dollar has a purpose. Instead of wondering where money disappeared, you gain control over allocation decisions.

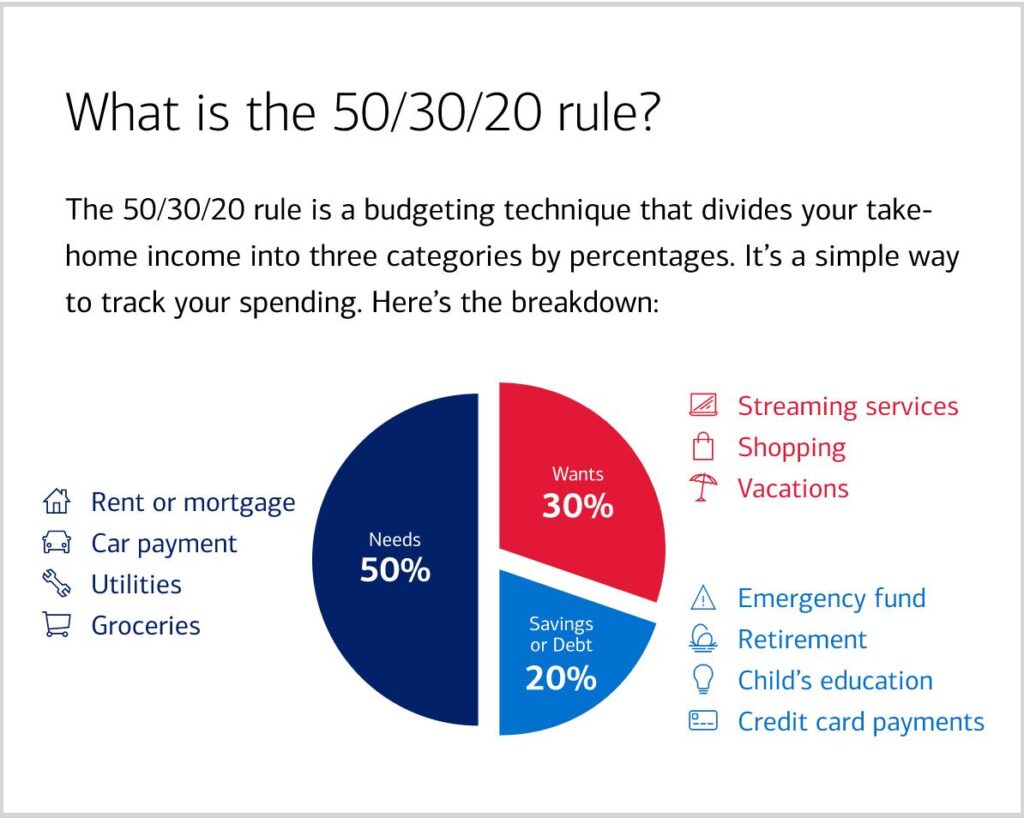

Using the 50/30/20 Budget to Save Money Fast

The popular 50/30/20 budgeting framework divides income into:

- 50% for necessities

- 30% for wants

- 20% for savings and debt repayment

For lower-income households, adjustments may be necessary. Essential expenses can exceed 50%, making it difficult to allocate 20% toward savings.

In such situations, focus on gradual improvement. Start by saving 5%, then increase to 10% as expenses decrease or income rises. The objective is progress rather than perfection.

A successful budget should remain flexible. Financial circumstances change, and your budget should adapt accordingly. Monthly reviews help ensure spending remains aligned with your goals.

Ways to Save Money Fast on a Low Income by Reducing Expenses

Reducing expenses is often the fastest way to improve savings because every dollar saved becomes immediately available for future goals.

The most effective cost-cutting strategies focus on major spending categories rather than small purchases alone.

Housing, transportation, food, utilities, and insurance typically represent the largest portions of household budgets. If utility bills are consuming a large portion of your income, learning how to save money on utilities can create additional monthly savings. Even modest reductions in these areas can generate substantial savings.

For example, negotiating lower insurance premiums, refinancing loans, finding more affordable housing, or reducing utility usage can create recurring monthly savings without significantly affecting quality of life.

Cut Daily Expenses to Save Money Faster

Saving money does not necessarily require extreme frugality. Instead, focus on eliminating expenses that provide little value.

Examples include:

- Unused subscriptions

- Frequent food delivery

- Impulse online purchases

- Premium service upgrades

- Brand loyalty without price comparison

Additional strategies include:

- Meal planning

- Buying generic products

- Shopping with lists

- Using coupons and cashback apps

- Purchasing second-hand items when appropriate

Small adjustments across multiple categories often create substantial cumulative savings while maintaining a comfortable lifestyle.

Step-by-Step Guide to Save Money Fast on a Low Income

Building savings becomes easier when following a structured approach.

Step 1: Calculate Your Monthly Income

Determine exactly how much money enters your household each month after taxes. Include wages, freelance income, benefits, and other reliable sources.

Step 2: Track Every Expense

Monitor spending for at least 30 days. Categorize expenses into housing, food, transportation, entertainment, debt payments, and miscellaneous purchases.

Step 3: Identify Quick Savings Opportunities

Look for expenses that can be reduced immediately, such as subscriptions, dining out, convenience purchases, and unused memberships.

Step 4: Set a Specific Savings Goal

Rather than saving without direction, establish a measurable objective.

Examples include:

- $500 emergency fund

- $1,000 emergency reserve

- Three months of living expenses

- Debt payoff target

Step 5: Automate Savings

Automatic transfers eliminate reliance on willpower. Schedule transfers immediately after payday so savings occur before spending decisions.

Step 6: Increase Income Where Possible

Even small income boosts accelerate progress significantly. Along with cutting expenses, finding ways to earn more money can help you reach your savings goals much faster. Consider freelance work, tutoring, pet sitting, online services, or weekend side jobs.

Expense Comparison for Low-Income Money Saving Strategies

| Expense Category | Average Monthly Cost | Potential Savings |

|---|---|---|

| Streaming Services | $40 | $20–$40 |

| Dining Out | $200 | $100–$150 |

| Utility Bills | $150 | $20–$50 |

| Grocery Spending | $500 | $50–$100 |

| Transportation | $300 | $30–$100 |

| Insurance | $150 | $20–$50 |

Reducing costs across several categories can create hundreds of dollars in monthly savings.

Real Examples of People Saving Money Fast on a Low Income

Real examples demonstrate that saving on a low income is achievable.

Example 1: Single Worker Saving an Emergency Fund

A retail employee earning $2,200 monthly tracked expenses and discovered $180 spent on convenience purchases. By reducing those expenses and automating weekly transfers, they saved $1,000 within five months.

Example 2: Family Reducing Grocery Costs

A family of four used meal planning, bulk purchases, and store-brand products to lower grocery spending by $150 monthly. The savings were redirected into an emergency fund and debt repayment plan.

Example 3: Side Income Accelerating Progress

A customer service representative earned an additional $250 monthly through freelance work. Instead of increasing spending, all extra income was deposited into savings, resulting in more than $3,000 accumulated within a year.

Benefits of Learning How to Save Money Fast on a Low Income

Building savings provides benefits beyond financial security.

First, savings reduce stress and anxiety. Financial uncertainty affects mental health, relationships, and overall quality of life.

Second, savings improve flexibility. Having cash reserves allows you to make decisions based on long-term goals rather than immediate financial pressures.

Third, savings create opportunities. Whether investing, starting a business, pursuing education, or purchasing a home, financial reserves expand future options.

Building savings is one of the most effective ways to improve your overall financial wellness.

Long-Term Financial Advantages

Over time, savings become the foundation of wealth building.

Emergency funds prevent debt accumulation. Reduced debt frees up cash flow. Increased cash flow allows for investing. Investing generates long-term growth.

This progression demonstrates how small savings habits can eventually support significant financial goals.

Challenges When Trying to Save Money Fast on a Low Income

While saving is essential, it is important to recognize limitations.

Individuals with extremely low incomes may struggle to save substantial amounts due to basic living expenses. In such situations, increasing income may be as important as reducing spending.

Unexpected emergencies can also delay progress. Medical expenses, job loss, and inflation may temporarily reduce savings capacity.

Balancing Savings With Essential Needs

Saving aggressively should never compromise necessities.

Avoid strategies that eliminate:

- Adequate nutrition

- Healthcare

- Safe housing

- Essential transportation

The goal is sustainable financial improvement rather than short-term deprivation.

Common Mistakes That Prevent Fast Saving on a Low Income

Many people unknowingly undermine their progress through avoidable mistakes.

Common errors include:

- Not tracking expenses

- Saving inconsistently

- Relying solely on willpower

- Ignoring small purchases

- Failing to set goals

- Carrying high-interest debt

- Lifestyle inflation after income increases

Why Lack of Planning Creates Financial Problems

Without a clear plan, money tends to disappear into daily spending.

Specific goals create accountability and motivation. Whether saving for emergencies, debt repayment, or future investments, a defined target improves decision-making and long-term commitment.

Expert Tips to Save Money Fast on a Low Income

Financial professionals consistently emphasize behavior over income when discussing savings success.

Research and experience show that disciplined habits often outperform complex financial strategies.

Experts recommend:

- Automating savings

- Tracking expenses weekly

- Prioritizing emergency funds

- Avoiding lifestyle inflation

- Increasing financial literacy

- Building multiple income streams

Over the long term, developing passive income streams can provide additional financial security and support consistent saving habits.

The Power of Small Financial Wins

Celebrating small milestones improves motivation.

Saving the first $100, $500, or $1,000 builds confidence and reinforces positive behaviors. These small victories often lead to larger financial achievements over time.

Frequently Asked Questions

1. Can I save money while living paycheck to paycheck?

Yes. Even small amounts saved consistently can create meaningful progress over time.

2. How much should I save each month?

Aim for at least 5–20% of income, depending on your financial situation.

3. What is the fastest way to save money?

Reducing major expenses and automating savings typically produce the fastest results.

4. Should I save or pay off debt first?

High-interest debt should often be prioritized after establishing a small emergency fund.

5. Is budgeting necessary?

Yes. Budgeting helps identify spending leaks and supports better financial decisions.

6. How large should an emergency fund be?

Most experts recommend three to six months of living expenses.

7. Are side hustles worth it?

For many people, side income significantly accelerates savings goals.

8. What if my income is extremely low?

Focus on essential expense reduction while exploring opportunities to increase earnings.

9. How can I avoid spending temptations?

Use automation, spending limits, and separate savings accounts.

10. How long does it take to build savings?

The timeline varies, but consistency matters more than speed.

Final Verdict

Learning how to save money fast on a low income is less about earning more and more about managing resources strategically. By creating a realistic budget, reducing unnecessary expenses, automating savings, avoiding debt traps, and increasing income where possible, anyone can make meaningful financial progress.

The most successful savers focus on consistent habits rather than dramatic changes. Even small amounts saved regularly can grow into a strong emergency fund, reduce financial stress, and create opportunities for future wealth building.

Start with one change today, automate the process, and build momentum. Over time, those small decisions can transform your financial future.