Saving money is one of the most important financial skills anyone can develop, yet many people still struggle with how to save money consistently. Rising living costs, lifestyle inflation, unexpected expenses, and easy access to credit often make it difficult to set aside funds for the future.

The good news is that saving money does not require a high income, extreme frugality, or complicated financial strategies. Instead, successful saving is usually the result of small, consistent decisions repeated over time. Whether your goal is building an emergency fund, paying off debt, buying a home, funding education, or achieving financial independence, a structured savings plan can help you reach those goals faster.

In today’s digital economy, there are more opportunities than ever to automate savings, reduce unnecessary spending, optimize budgets, and make smarter financial decisions. However, many people focus on cutting small expenses while overlooking larger financial leaks that have a greater impact on long-term wealth.

This guide explains how to save money effectively, avoid common mistakes, create sustainable habits, and build a financial system that supports both your current lifestyle and future goals.

Quick Answer

The most effective way to save money is to track your expenses, create a realistic budget, automate savings, reduce unnecessary spending, avoid lifestyle inflation, build an emergency fund, and consistently save a percentage of every paycheck before spending on non-essential items.

Key Takeaways

- Pay yourself first by automating savings.

- Track every expense to identify spending leaks.

- Follow a budget that matches your income and goals.

- Build an emergency fund covering 3–6 months of expenses.

- Eliminate high-interest debt as quickly as possible.

- Avoid lifestyle inflation when income increases.

- Use financial apps and automation to stay consistent.

- Focus on long-term habits rather than short-term sacrifices.

- Prioritize major savings opportunities such as housing, transportation, and debt reduction.

- Consistency matters more than income level.

Table of Contents

- Why Saving Money Matters

- Understanding Where Your Money Goes

- How to Save Money Step by Step

- Smart Money-Saving Strategies

- Budgeting Methods Compared

- Real-World Examples

- Benefits of Saving Money

- Risks and Limitations

- Common Money-Saving Mistakes

- Expert Insights

- FAQs

- Final Verdict

Why Saving Money Matters

Saving money is not simply about accumulating cash in a bank account. It is about creating financial flexibility, reducing stress, and giving yourself more choices in life. People who maintain healthy savings often experience greater financial stability because they are better prepared for emergencies, economic downturns, medical expenses, job loss, and major life changes.

One of the biggest advantages of saving money is the ability to handle unexpected situations without relying on high-interest credit cards or personal loans. A sudden car repair, medical bill, or home maintenance issue can become a financial crisis for someone living paycheck to paycheck. For someone with savings, the same expense becomes manageable.

Savings also serve as the foundation for wealth building. Before investing in stocks, mutual funds, real estate, or retirement accounts, individuals should establish strong savings habits. Savings provide liquidity, while investments provide growth.

Another important benefit is psychological. Financial stress is one of the leading causes of anxiety among adults worldwide. Having a dedicated savings fund can provide peace of mind and improve overall well-being, which is an important aspect of financial wellness.

In addition, saving money creates opportunities. Whether you want to start a business, switch careers, take a sabbatical, purchase a home, or pursue higher education, savings give you options that would otherwise be unavailable.

Many people believe they need a large income to save effectively. In reality, saving is primarily a behavioral skill. While higher income certainly helps, many high earners struggle financially because they spend everything they make. Meanwhile, individuals with moderate incomes often build substantial savings through discipline and consistency.

The true purpose of saving money is not deprivation. It is creating a financial system that supports your future goals while allowing you to enjoy life responsibly in the present.

Understanding Where Your Money Goes

Before you can save more money, you need a clear understanding of your current spending habits. Many people underestimate how much they spend each month because they focus only on major expenses and ignore smaller purchases that accumulate over time.

Track Every Expense

The first step is to monitor all spending for at least 30 days. Review bank statements, credit card transactions, digital wallet payments, subscriptions, and cash purchases. Categorize expenses into housing, transportation, food, utilities, entertainment, debt payments, insurance, healthcare, and miscellaneous spending.

This process often reveals surprising patterns. For example, daily food delivery, subscription services, impulse purchases, and convenience spending can quietly consume hundreds of dollars each month.

Identify Fixed and Variable Expenses

Fixed expenses remain relatively constant each month, including rent, mortgage payments, insurance premiums, and loan payments. Variable expenses fluctuate, such as dining out, entertainment, travel, and shopping.

Understanding this distinction is important because variable expenses usually provide the easiest opportunities for immediate savings. However, long-term financial improvement often comes from optimizing major fixed expenses such as housing and transportation.

Calculate Your Savings Rate

Your savings rate is the percentage of income that you save each month. Financial experts often recommend saving at least 20% of after-tax income, although the ideal rate depends on your goals, age, and financial obligations.

For example:

- Monthly income: $4,000

- Monthly savings: $800

- Savings rate: 20%

Tracking this metric helps measure progress more effectively than focusing only on dollar amounts.

Analyze Spending Triggers

Many spending decisions are emotional rather than logical. Stress, boredom, social pressure, and convenience frequently influence purchasing behavior.

Identifying personal spending triggers allows you to develop strategies that reduce impulsive purchases. Simple actions such as waiting 24 hours before buying non-essential items can significantly reduce unnecessary spending.

Understanding where your money goes creates awareness, and awareness is the foundation of every successful savings plan.

How to Save Money Step by Step

Creating a sustainable savings strategy requires more than simply spending less. It involves building a system that consistently directs money toward your financial goals.

Step 1: Set Clear Savings Goals

Specific goals create motivation and direction. Instead of saying, “I want to save more money,” define measurable objectives.

Examples include:

- Save $5,000 for an emergency fund.

- Save $20,000 for a home down payment.

- Save $10,000 for travel.

- Save $100,000 for retirement investments.

Clear goals make progress easier to track.

Step 2: Create a Realistic Budget

A budget is a spending plan, not a restriction. One popular framework is the 50/30/20 rule:

- 50% for necessities

- 30% for wants

- 20% for savings and debt repayment

Adjust percentages according to your circumstances while ensuring savings remain a priority.

Step 3: Pay Yourself First

One of the most effective financial principles is paying yourself before spending on discretionary items. Schedule automatic transfers to savings accounts immediately after receiving income.

Automation removes the temptation to spend money before saving it.

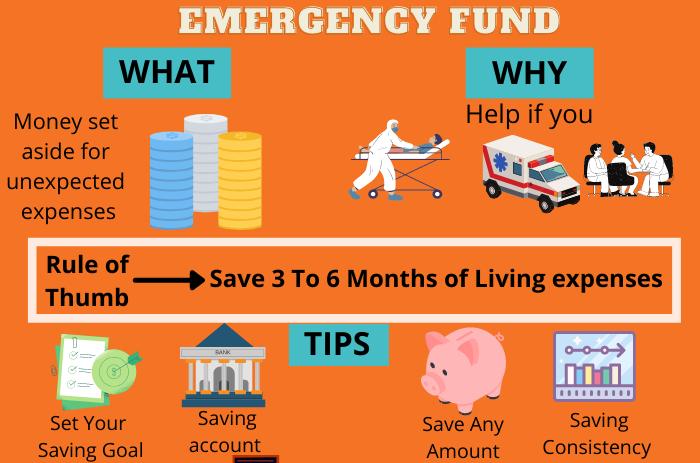

Step 4: Build an Emergency Fund

Emergency funds provide protection against unexpected financial setbacks. Most experts recommend maintaining three to six months of essential living expenses.

Start with a smaller milestone such as $1,000 and gradually expand the fund over time.

Step 5: Reduce High-Interest Debt

High-interest debt can undermine saving efforts because interest costs often exceed investment returns.

Prioritize:

- Credit card debt

- Payday loans

- Personal loans with high rates

Reducing debt improves cash flow and accelerates future savings.

Step 6: Increase Income

Savings growth is not limited to expense reduction. Additional income from freelancing, side businesses, consulting, tutoring, or part-time work can significantly increase savings capacity. Learning how to earn more money can help you accelerate your savings goals and build long-term financial security.

Step 7: Review Progress Monthly

Financial situations change regularly. Monthly reviews help identify areas for improvement and ensure you remain aligned with your goals.

The key is consistency. Small actions repeated for years create significant financial results.

Smart Money-Saving Strategies

Beyond budgeting, several advanced strategies can dramatically improve your ability to save money.

Reduce Major Expenses First

Many people focus on small daily expenses while ignoring larger costs. Housing, transportation, and debt typically represent the largest portions of most budgets.

Potential strategies include:

- Negotiating rent

- Refinancing loans

- Downsizing housing

- Using public transportation

- Reducing vehicle ownership costs

A single adjustment in a major expense category can save thousands annually.

Automate Financial Decisions

Automation reduces decision fatigue and increases consistency.

Examples include:

- Automatic savings transfers

- Automated bill payments

- Retirement account contributions

- Investment deposits

Removing manual effort improves long-term success rates.

Use Cash-Back and Rewards Strategically

Cash-back cards and rewards programs can provide value when used responsibly. However, rewards should never justify unnecessary spending.

The best approach is earning rewards on purchases you would make regardless.

Avoid Lifestyle Inflation

Lifestyle inflation occurs when spending rises proportionally with income increases.

Instead of spending every raise:

- Save part of salary increases.

- Increase investment contributions.

- Strengthen emergency reserves.

- Accelerate debt repayment.

Maintaining previous spending levels while earning more can dramatically increase wealth accumulation.

Practice Intentional Spending

Saving money does not mean eliminating enjoyment. Intentional spending focuses on purchasing things that provide genuine value while eliminating expenses that do not.

Ask before every purchase:

- Do I need this?

- Will it improve my life?

- Is there a lower-cost alternative?

- Can I delay this purchase?

These simple questions often prevent unnecessary spending and improve financial decision-making.

Budgeting Methods Compared

| Budgeting Method | Best For | Advantages | Limitations |

|---|---|---|---|

| 50/30/20 Rule | Beginners | Simple and flexible | Less precise |

| Zero-Based Budget | Detailed planners | Maximum control | Time-consuming |

| Envelope System | Overspenders | Strong spending discipline | Less convenient digitally |

| Pay Yourself First | Savers | Prioritizes savings automatically | Requires consistency |

| Value-Based Budgeting | Goal-focused individuals | Aligns spending with priorities | Requires self-awareness |

The ideal budgeting method depends on personal preferences, income stability, and financial goals.

Real-World Examples

Example 1: New Graduate

A recent graduate earning $3,000 monthly decides to save 15% of income through automatic transfers. By saving $450 monthly, they accumulate $5,400 within a year without making drastic lifestyle changes.

Example 2: Family Household

A family reviews expenses and discovers they spend $500 monthly on subscriptions, dining out, and impulse purchases. Reducing those costs by half creates an additional $3,000 in annual savings.

Example 3: Mid-Career Professional

After receiving a $10,000 salary increase, a professional allocates 70% of the raise toward savings and investments. Over time, this strategy significantly accelerates retirement readiness without reducing quality of life.

These examples demonstrate that meaningful savings often result from intentional financial systems rather than extreme sacrifice.

Benefits of Saving Money

Saving money provides advantages that extend far beyond financial security.

The most immediate benefit is improved resilience during emergencies. Unexpected expenses become manageable rather than catastrophic.

Savings also reduce dependence on debt. Individuals with cash reserves are less likely to rely on credit cards or loans when facing financial challenges.

Another major benefit is increased freedom. Savings can support career transitions, entrepreneurship, education, relocation, or early retirement.

Long-term wealth creation is another significant advantage. Savings provide capital that can later be invested in assets that generate returns, compound growth, and even create passive income over time.

Financial confidence also improves. People with savings often experience lower stress levels and greater confidence in decision-making because they are not operating under constant financial pressure.

Finally, savings help individuals pursue opportunities rather than merely reacting to problems. Whether investing in a business, purchasing a property, or taking advantage of market opportunities, having available capital creates options that others may miss.

Risks and Limitations

While saving money is beneficial, there are limitations to consider.

Excessive saving can sometimes prevent individuals from enjoying life or investing in personal development. Financial planning should balance future security with present well-being.

Inflation presents another challenge. Money held in low-yield accounts may lose purchasing power over time if inflation exceeds interest earnings.

There is also an opportunity cost associated with keeping too much cash. Once emergency funds are established, additional funds may be better allocated toward long-term investments depending on risk tolerance and goals.

Another limitation is income constraints. For some households, rising living expenses and limited earnings create genuine barriers to saving. In these situations, increasing income may be as important as reducing expenses.

The goal is not maximizing savings at all costs but building a balanced financial strategy that supports both short-term needs and long-term objectives.

Common Money-Saving Mistakes

Many people struggle to save because they repeat common financial mistakes.

The first mistake is saving whatever remains after spending. Successful savers reverse the process by saving first and spending the remainder.

Another mistake is setting unrealistic budgets. Extreme restrictions often lead to frustration and abandonment.

Ignoring small recurring expenses can also be costly. Subscription services, fees, and impulse purchases frequently accumulate into significant annual costs.

Many individuals focus exclusively on cutting expenses while neglecting income growth opportunities. Increasing earning potential can often have a greater impact than minor spending reductions.

Failing to establish an emergency fund is another common error. Without one, unexpected expenses often result in debt accumulation.

Finally, many people underestimate the effects of lifestyle inflation. Increased earnings should improve savings rates, not simply fund higher spending.

Avoiding these mistakes dramatically improves long-term financial outcomes.

Expert Insights

Financial planners consistently emphasize that behavior matters more than complex financial products.

Research across personal finance studies shows that automatic savings systems significantly improve long-term outcomes. When savings occur automatically, individuals are less likely to rely on willpower.

Experts also recommend focusing on high-impact financial decisions. Housing, transportation, taxes, insurance, and debt typically have a greater effect on wealth than minor daily expenses.

Another common recommendation is to create savings goals tied to specific outcomes. People save more effectively when they understand exactly what they are working toward.

Financial professionals also emphasize the importance of consistency. Saving modest amounts regularly often produces better results than attempting occasional large contributions.

Ultimately, successful saving is less about perfection and more about creating repeatable habits that support long-term financial health.

FAQs

1. What is the fastest way to save money?

The fastest approach combines expense reduction, debt repayment, and income growth while automating savings contributions.

2. How much money should I save each month?

A common recommendation is saving at least 20% of after-tax income, though individual circumstances vary.

3. Should I save money or pay off debt first?

Generally, build a small emergency fund first, then prioritize high-interest debt repayment.

4. How large should an emergency fund be?

Most financial experts recommend three to six months of essential living expenses.

5. Is budgeting necessary to save money?

While not mandatory, budgeting significantly improves savings consistency and financial awareness.

6. What are the biggest spending categories to optimize?

Housing, transportation, food, insurance, and debt payments typically offer the largest savings opportunities.

7. How can I save money on a low income?

Focus on budgeting, eliminating unnecessary expenses, increasing income opportunities, and automating even small savings amounts. You can also explore practical strategies to save money fast on a low income if you’re working with limited financial resources.

8. Why do people struggle to save money?

Common reasons include lifestyle inflation, lack of budgeting, impulsive spending, debt, and unclear financial goals.

9. Should I keep all savings in a bank account?

Emergency funds should remain accessible, while long-term funds may be invested according to risk tolerance and goals.

10. How long does it take to build substantial savings?

The timeline depends on income, savings rate, and financial goals, but consistency is the primary factor.

Final Verdict

Learning how to save money is one of the most valuable financial skills you can develop. Effective saving is not about deprivation or extreme frugality. It is about creating systems that align spending with your priorities, protect you from financial emergencies, and help you achieve long-term goals.

The most successful savers focus on consistency, automation, intentional spending, and continuous improvement. By understanding where your money goes, establishing clear goals, building an emergency fund, and avoiding common mistakes, you can create lasting financial stability and future wealth.

The best time to start saving money is today—even if you begin with a small amount.